Q1 2022 closed out this week making it the worst quarter for the US markets since the pandemic hit back in Q1 2020. However, for the past 3 weeks, markets have been pushing higher from their lows set back in late February of this year. The S&P was down -13% for the year and did an about-face to rally by +10%. However, markets this week were in a consolidation pattern after moving higher in such a short time period. The Russell 2000 was the winner this week where it eked out +0.62%.

Big Picture

Starting off this week, markets rallied higher for the better part of Monday and Tuesday. But with such a strong rally (in the past couple of weeks), the market gave back with a reversal as the S&P, Nasdaq, DJIA, and Russell closed out the week on modest gains. The image below shows price movement after hitting the lows on February 24, 2022. Markets rallied up to 38.2% on the Fibonacci level and then corrected into support during mid-March. And in terms of short time span, markets then had one of the strongest rallies to close out March 2022. Markets pushed up to challenge the 61.8% Fibonacci level.

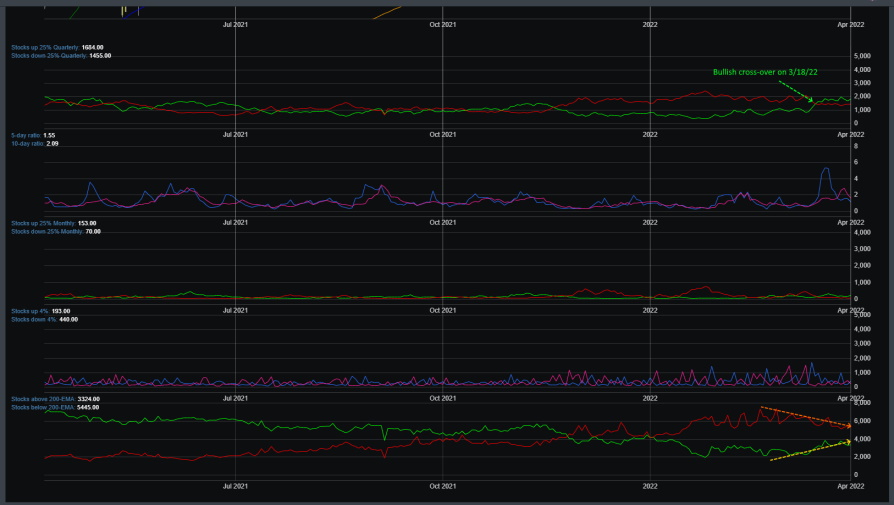

Overall, markets on the larger time frame are still bearish as can be seen in the image below. But the intermediate time frame is suggesting a strong bullish reading that may start pushing the overall trend to higher. Right now, the daily reading is suggesting consolidation or some downward pressure. But given the strong intermediate trend, this is most likely short-lived.

Market Breadth

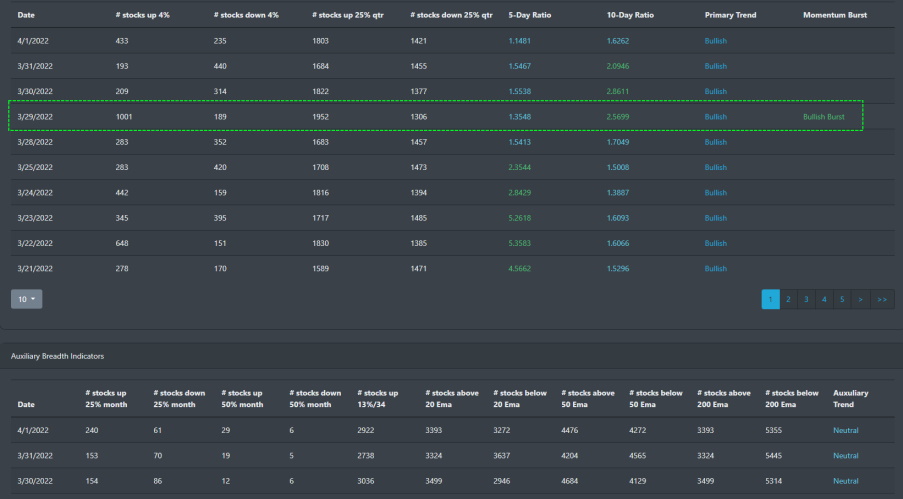

For the past year, market breadth has been slowly deteriorating. We discussed this in many of our prior blogs. On 11/30/2021 and 1/18/22, the bearish signal triggered which suggests a change in market dynamics to the downside. Now, markets are looking to make the switch to the bullish side.

On 3/18, market breadth crossed over to the bullish side. And now, markets are looking poise to move higher as the bullish signal was triggered this week. This is a typical intermediate indicator that suggests that there can still be downward pressure but overall markets are expected to rally higher in the coming weeks. Stocks above and below their 200 EMAs are also trending in the direction that suggests improving market internals.

Market Sentiment

With market sentiment being in the fear mode for most of Q1 2022, the bears were looking take control of 2022. But just as we discussed in our blogs before this, we said to buy the dip. Market internals started reversing to the bullish side and in a matter of less than a month, markets rallied off of their February lows to eclipse both the 50 and 200 DMA. With such a sharp move higher, we expect the next move to be a consolidation and move lower before markets continue their rally to challenge the previous highs.

Economic Outlook

This Friday, the 10-year Treasury closed around 2.38%. The 2-year Treasury inched higher to close on Friday at 2.44%. This inversion of the yield curve typically means that the short-term debt (2-year treasury) provides a higher yield than the long-term investment (10-year term). For many investors, this historically signals a probability that a recession is on the horizon. The last time the 10-2 yield spread inverted was back in 2019 and historically a recession preceded 9 out of 10 times since 1955. To be honest, we are far from a recession and if we look at the 3-month vs 10-year curve, there is about a +180 basis point spread. So, clearly, there is a low probability that we are seeing a potential for a recession in the next year or two. For BullGap's recession index, a recession is potentially on the horizon when the index encroaches above 40.

Market Outlook

The larger time frames still suggest strong downward pressure on the markets. However, just recently, the intermediate bullish signals were triggered. This week, markets had a technical sell-off where markets consolidated after having a sharp rally to close out March 2022. Let's look at the markets from the bigger time frame using our TrendFinder tool.

SPY

Below is SPY with the monthly trigger signals in green and red. When a monthly buy signal (green with M label) triggers, we historically have a strong rally that can last months if not years. Here we can see how powerful and accurate these triggers can be. There was a monthly sell trigger on 2/3/202 that indicated strong selling pressure to come. This trigger occurred right before the crash of March 2020. Additionally, there was a strong monthly buy signal on 5/3/2020. We know what happened since then - one of the strongest rallies in a 2-year time span for SPY. Now, this week, while markets were consolidating, we just received our most recent monthly buy signal on 4/1/2022.

QQQ

QQQ also has a similar pattern to SPY. But unlike SPY, there has yet to be a monthly buy signal for the Nasdaq ETF. The most recent signal monthly signal was a sell signal on 1/3/2022. QQQ dropped since 1/3/2022 triggered but has recently rallied to break through its first key resistance at the 363 region. We expect a monthly buy signal to trigger in the coming weeks.

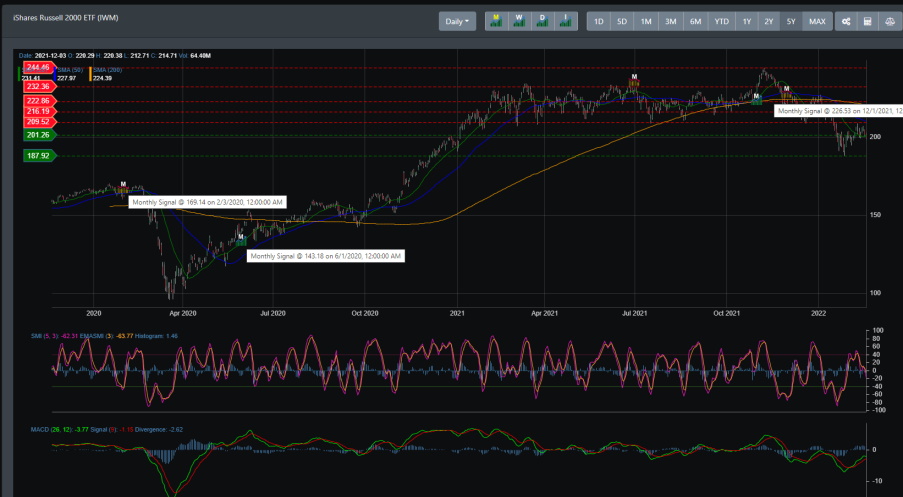

IWM

Like SPY, there was a monthly sell signal on 2/3/2020 that suggested a big move down was coming. That occurred right before the March drop in 2020. For this year, IWM has been trending lower since hitting its most recent monthly sell signal. That signal occurred on 12/1/2021. Like QQQ, the intermediate signals are turning bullish and we expect a monthly buy signal to trigger in the coming weeks.

Concluding

After correcting for most of Q1 2022, markets rallied to end March on a strong note. Markets are now consolidating those gains. This is natural and quite healthy for a bull market. Investors and traders are taking profit and looking to take new positions. Though we see some downward pressure on the near-term charts, the intermediate market readings are bullish which suggests a strong rally is about to hit the markets.