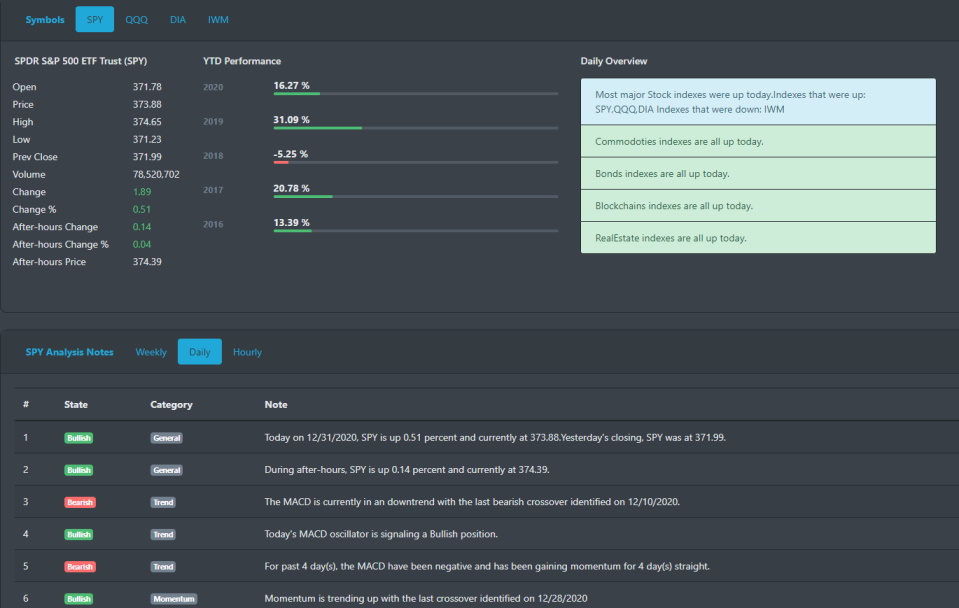

Let's face it. The "Santa Claus" rally that started last week and wraps up this week has thus far been moderately bullish. While historically, the last week of December should have been on the side of the bulls, it was rather a volatile and choppy week. SPY just closed a little over .85% higher than its previous high which was set back in mid-December. For the indexes, S&P 500 and Dow Jones both closed the year-end at fresh new highs. Nasdaq rallied to a gain of 0.74% and posted a record high. Russell 2000 for the week dropped over 1.45%.

Big Picture

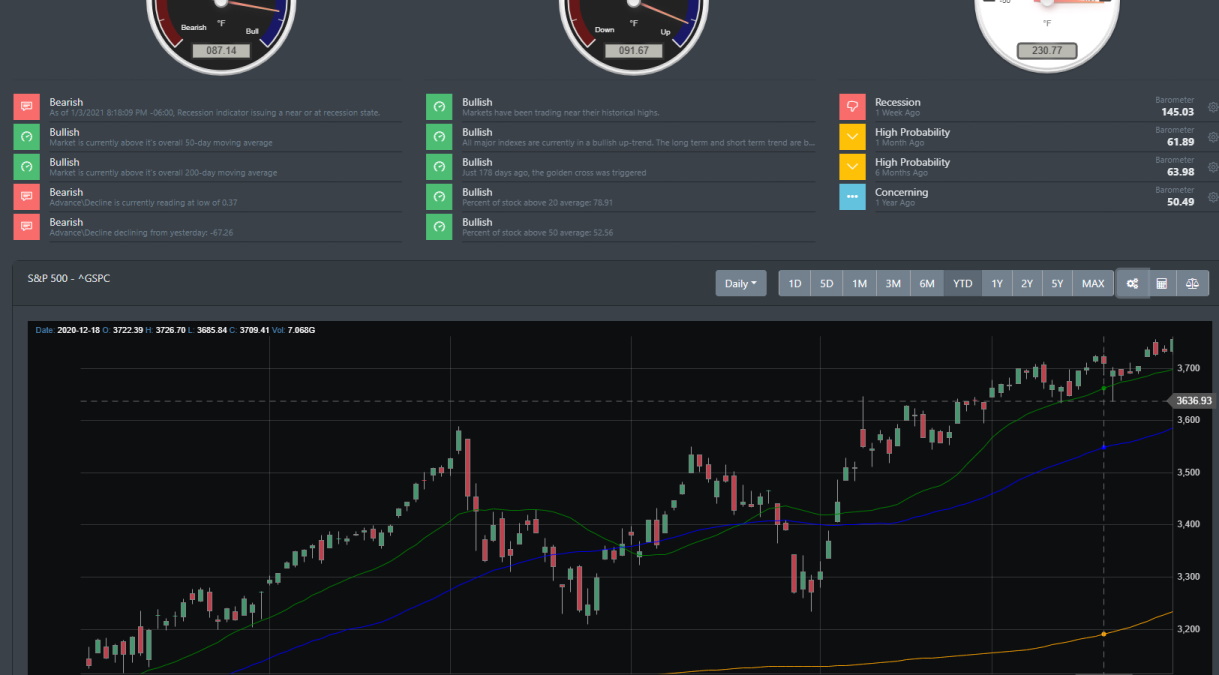

On Friday, the market did close up just a bit but for most of last week, it has been quite volatile. That said, the market is clearly in a bullish state and it seems that stocks are clearly looking ahead to better days. Days where covid vaccination rollout reaches the masses, economic relief becomes available and the economy reopens.

Right now, market momentum is still in favor of the bulls though.

Market Breadth

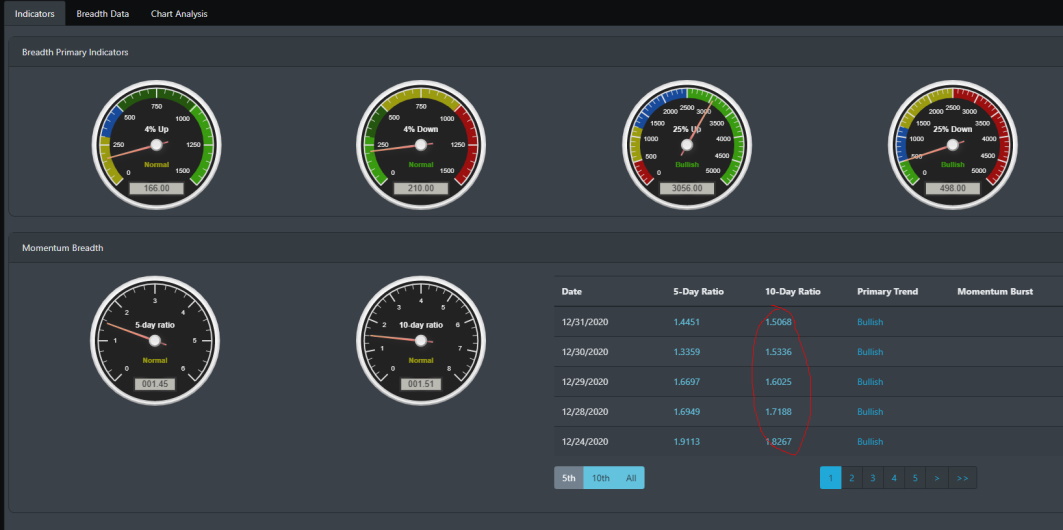

Though momentum has been in overdrive for the past couple of months, it has slowed down. We can see that in the chart below where the 10-day ratio (representing the last 10 days of 4% plus and down breakouts) has been showing some slowdown.

Market breadth is still bullish with the last momentum burst being signaled on 12/16/2020. It could be that the markets are in a consolidation pattern. However, it could also be that the market is looking too far ahead and have priced in all the good news.

Economic Outlook

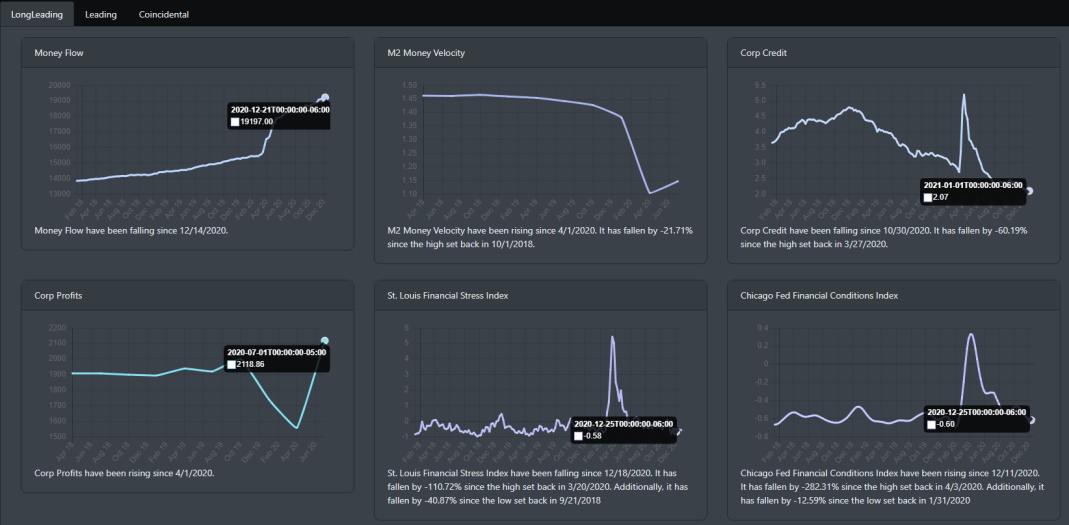

Constant liquidity injections from global central banks have led to a major rebound in the equity market. The U.S major stock indexes are now trading at all-time highs. As evident in the screenshot below, money flow has increased significantly in the past 9 months. Credit is at all-time lows which allows corporations to borrow and invest. And after June 2020, corporate profits are above pre-pandemic levels.

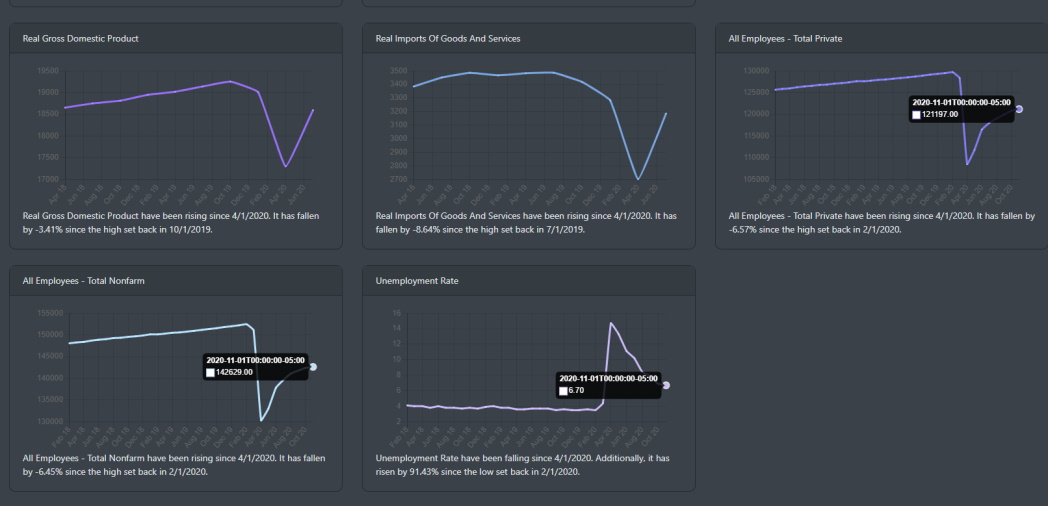

Employment though is a different story. Ever since bottoming out near April and June 20, the All Employees total private and nonfarm still not recovered from pre-COVID levels and current readings are suggesting a slowing down of job growth. Though this week, claims did fall down to 787K, the unemployment rate is historically high at 6.7%.

Market Outlook

Last week, markets closed on a high note. New highs after new highs have been a common occurrence for this December.

Concluding

Despite the market heading higher, valuations are looking stretched out. With sentiment indicators trading at high levels and P\E ratios starting to diverge from their historical levels, investors seem to be all in on the market. With everyone in and buying to push the market higher, the question comes as to when we will see a topping with no buyers left willing to buy stocks at such a high price. For now and at least in the short term, liquidity is still the name of the game and may propel the S&P 500 into 4000 sometime this year.